AI governance in financial regulation is the structured system of policies, controls, and accountability mechanisms that financial institutions use to deploy AI safely, ethically, and in compliance with applicable law. The industry term for this discipline is "AI governance," and it encompasses everything from model risk management to data protection obligations under frameworks like the EU AI Act, NIST AI RMF, and the Financial Stability Board's sound practices. For compliance officers and financial regulators, getting this right is not optional. Regulators are moving from guidance to enforcement, and institutions that lack documented controls face penalties, reputational damage, and operational disruption.

What are the core components of an AI governance framework?

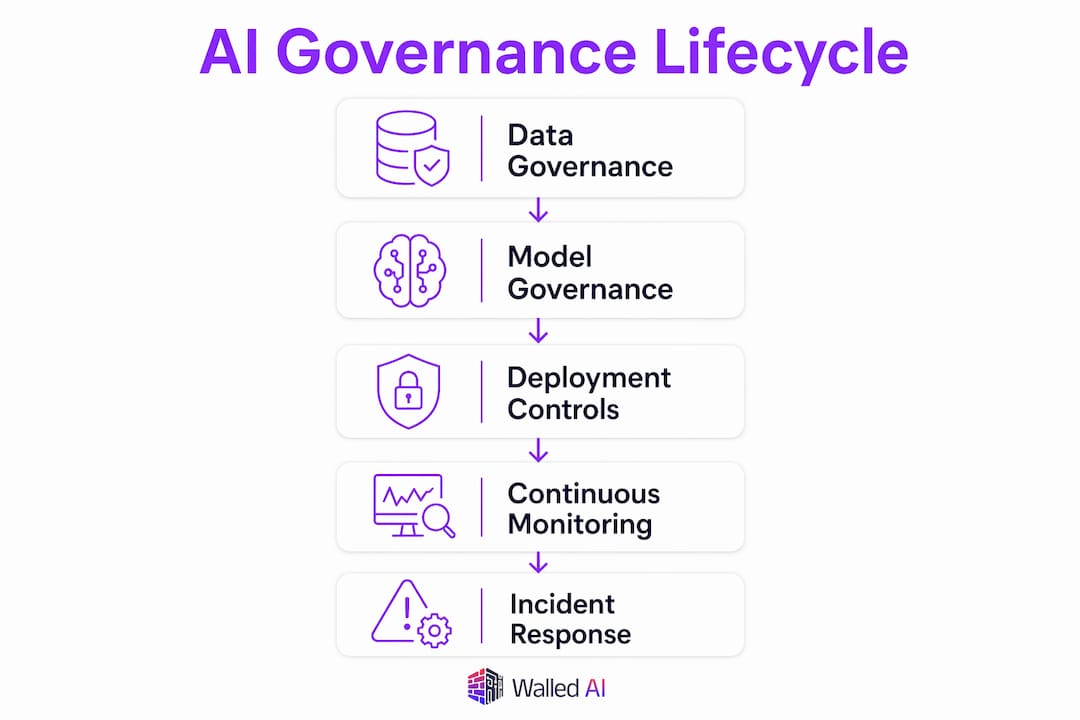

A mature AI governance framework contains 15 controls across five lifecycle categories: data governance, model governance, deployment controls, monitoring, and incident response. Each category addresses a distinct phase of an AI system's life, from the moment training data is collected to the point where a model is retired. Together, these controls close the gaps that expose organizations to regulatory penalties and security risks.

Data governance controls

Data governance controls cover data lineage tracking, consent verification, and sensitivity classification. Compliance officers need to know exactly where training data originated, whether it was collected lawfully, and whether it contains regulated personal data subject to GDPR or PDPA. Without this foundation, every downstream model inherits the same legal exposure.

Model governance controls

Model governance covers the model inventory, version control, and validation records. Every AI system deployed in a financial institution should appear in a centralized registry with its risk classification, intended use, and approval status. This registry is not a formality. Auditors treat it as primary evidence that the institution knows what AI it is running and who approved it.

Deployment, monitoring, and incident response

Deployment controls define which environments an AI system can operate in and what data it can access. Monitoring controls require continuous logging of AI outputs, drift detection, and performance thresholds. Incident response controls specify how anomalies are classified, escalated, and remediated. The EU AI Act classifies credit scoring and insurance AI as high risk, which means these three control categories carry mandatory audit and documentation requirements for a large share of financial AI deployments.

- Data lineage tracking: Records the origin, transformation, and movement of all training and inference data.

- Human-in-the-loop review: Defines where a human must review or approve an AI decision before it takes effect.

- Audit logging: Creates immutable records of model inputs, outputs, and decisions for regulatory inspection.

- Incident classification: Categorizes AI failures by severity so escalation paths are clear and response times are measurable.

- Model inventory: Maintains a live register of all AI systems, their risk tier, owners, and approval history.

Pro Tip: Build your model inventory before your next regulatory examination, not during it. Auditors who find an undocumented AI system in production treat it as a control failure, regardless of how well the system actually performs.

Who holds accountability in AI governance for financial compliance?

Diffuse accountability is the primary governance failure in financial institutions. When responsibility for an AI system is shared across multiple teams with no named owner, no one has the authority to approve risk acceptance, order remediation, or sign off on audit findings. Successful institutions assign a single accountable owner to each AI system, supported by a cross-functional governance committee that advises but does not decide.

Governance committee composition

A governance committee for AI in financial services typically includes the Chief AI Officer (CAIO), the Chief Risk Officer (CRO), the Chief Technology Officer (CTO), the Chief Compliance Officer, and representatives from legal and data protection. The committee sets policy, reviews high-risk deployments, and escalates systemic issues to the board. It does not replace the named owner of each AI system.

Roles and their distinct responsibilities

- Chief AI Officer: The CAIO manages the AI system registry and lifecycle governance, linking technical teams with executive leadership. The CAIO is accountable to the board for the institution's overall AI governance posture.

- Chief Compliance Officer: Monitors regulatory developments, maps AI deployments to applicable obligations, and owns the compliance reporting workflow. This role is the primary contact for regulators during examinations.

- Chief Risk Officer: Classifies AI systems by risk tier, approves risk acceptance decisions, and owns the escalation protocol for AI incidents that cross defined thresholds.

- Business unit owners: Manage the specific context and data exposure of each AI application within their domain. They accept operational risk for their use cases and cannot delegate that acceptance to a central team.

- Platform owners: Govern the runtime environment, baseline security controls, and infrastructure on which AI systems operate. Platform owners manage infrastructure security while business owners manage decision context. This separation is critical for regulatory compliance because it prevents both parties from assuming the other has covered a given control.

Pro Tip: When onboarding a third-party AI vendor, require a contractual clause that names the vendor's accountable owner for the AI system and specifies their obligations for incident notification, audit cooperation, and control evidence. Generic vendor agreements rarely include this, and regulators will ask for it.

How should financial institutions manage AI-related risks?

AI risk management in financial services follows a four-stage lifecycle: assessment, mitigation, monitoring, and incident handling. The FSB's 12 sound practices for responsible AI adoption cover all four stages, addressing organization-wide governance, development and deployment risks, and AI-specific cybersecurity and third-party risks. These practices are designed to complement existing standards rather than replace them, which means compliance officers can map them directly onto current GRC frameworks.

Risk assessment and classification

Every AI system should receive a risk classification before deployment. Classification criteria include the sensitivity of data processed, the reversibility of AI-driven decisions, the degree of human oversight, and the regulatory category of the use case. High-risk systems under the EU AI Act require a conformity assessment, technical documentation, and a post-market monitoring plan before they go live.

Continuous monitoring and audit trails

Continuous monitoring means more than periodic model validation. It requires real-time logging of AI inputs and outputs, automated drift detection, and threshold-based alerts that trigger human review. Governance defines permitted AI actions, the points where human review is mandatory, and the audit requirements that apply at each stage. Immutable audit logs are the primary evidence regulators examine when assessing whether an institution's AI controls actually operated as described in policy documents.

| Risk category | Key control | Regulatory reference |

|---|---|---|

| Data protection | Automated sensitivity classification and masking | GDPR, PDPA |

| Model accuracy | Human-in-the-loop review for high-stakes decisions | EU AI Act, NIST AI RMF |

| Cybersecurity | API security controls and prompt injection defense | FSB sound practices |

| Third-party AI | Vendor contract oversight and audit rights | FSB sound practices |

| Incident response | Named escalation path and classification protocol | MAS TRM, EU AI Act |

Pro Tip: Map your AI audit trail requirements to your existing records retention policy. Regulators under the EU AI Act expect documentation to be retained for at least 10 years for high-risk systems. Most institutions discover this gap only when preparing for their first AI-specific examination.

What practical steps can compliance officers take to implement AI governance?

Building an AI governance program starts with a complete inventory. Compliance officers cannot govern what they cannot see, and most financial institutions discover undocumented AI systems during their first formal inventory exercise. The inventory should capture the system name, owner, risk classification, data inputs, regulatory category, and current control status.

- Establish an AI registry: Create a centralized, living register of all AI systems in production and development. Assign a named owner and risk tier to each entry before the system goes live.

- Integrate with enterprise GRC: Map AI governance controls to your existing governance, risk, and compliance framework. This prevents parallel processes and makes AI risk visible in board-level risk reporting.

- Conduct pre-deployment risk assessments: Require a formal risk assessment for every new AI system before deployment. For high-risk systems under the EU AI Act, this assessment must include a conformity review and technical documentation package.

- Prepare for multi-jurisdictional obligations: Financial institutions operating across borders face overlapping requirements from the EU AI Act, GDPR, PDPA, MAS TRM, and the FSB's multi-jurisdiction coordination recommendations. Build a regulatory mapping table that shows which control satisfies which obligation across each jurisdiction.

- Test audit readiness continuously: Auditors require operational evidence, not just policies. Named owners must have documented authority for approvals, risk acceptance, and remediation. Run internal audit simulations quarterly to verify that evidence is available and current.

For institutions building or updating their enterprise AI governance framework, the 2026 regulatory environment rewards programs that treat governance as an operational discipline rather than a documentation exercise.

Key Takeaways

Effective AI governance in financial regulation requires named accountability, documented controls across the full AI lifecycle, and continuous audit readiness rather than periodic policy reviews.

| Point | Details |

|---|---|

| Assign named owners | Every AI system needs one accountable owner with authority to approve risk and order remediation. |

| Build a model inventory first | A centralized AI registry is the foundation auditors and regulators examine before anything else. |

| Apply lifecycle controls | Governance must cover data, model, deployment, monitoring, and incident response stages without gaps. |

| Separate platform and use-case accountability | Platform owners govern infrastructure; business owners govern decision context and data exposure. |

| Treat audit readiness as continuous | Operational evidence of control enforcement matters more to regulators than written governance policies. |

Where governance programs actually break down

The most common failure I see in financial institutions is not a missing policy. It is a policy that exists but has no operational owner. A governance committee can approve a framework document in the morning and have zero visibility into whether any of its controls are actually running by afternoon. That gap is where regulators find their findings.

The second failure is treating vendor AI as someone else's problem. When a financial institution deploys a third-party AI model for credit decisioning, the regulatory obligation stays with the institution. The vendor's indemnity clause does not satisfy the EU AI Act's conformity requirements or the FSB's third-party risk practices. Compliance officers who have not reviewed their vendor contracts against current AI governance obligations are carrying undisclosed regulatory exposure right now.

The fix is architectural, not procedural. Governance needs to be embedded in the systems that run AI, not just the documents that describe it. That means real-time policy enforcement, immutable logging, and automated alerts that fire when a control threshold is breached. A governance framework that requires a human to manually check compliance is a framework that will fail under examination pressure. The institutions that pass AI-specific regulatory reviews in 2026 are the ones that built governance into their AI infrastructure from the start, not the ones that added a policy layer on top of existing deployments.

— Rishabh

Walled supports AI governance for financial institutions

Financial institutions managing AI governance obligations across the EU AI Act, GDPR, PDPA, and MAS TRM need more than policy documentation. They need controls that operate in real time, at the point where AI systems process sensitive data.

Walled provides a unified AI control plane that enforces data loss prevention, prompt injection defense, and policy compliance across every AI interaction before data reaches a model. The platform generates immutable audit trails, supports on-premises and air-gapped deployments, and maps controls to specific regulatory obligations. Compliance officers managing AI governance for financial services can use Walled to close the gap between written governance policy and operational control enforcement, giving regulators the evidence they require.

FAQ

What is AI governance in financial regulation?

AI governance in financial regulation is the system of policies, controls, and accountability mechanisms that financial institutions use to deploy AI in compliance with applicable laws and regulatory frameworks, including the EU AI Act, GDPR, and FSB sound practices.

What are the key components of an AI governance framework?

A mature AI governance framework covers five categories: data governance, model governance, deployment controls, continuous monitoring, and incident response, with 15 controls distributed across these stages.

Who is accountable for AI governance in a financial institution?

A single named owner holds accountability for each AI system, supported by a cross-functional governance committee. The Chief AI Officer typically oversees the AI system registry and reports the institution's overall governance posture to the board.

How does the EU AI Act affect AI governance obligations in financial services?

The EU AI Act classifies credit scoring and insurance AI as high risk, requiring mandatory conformity assessments, technical documentation, and post-market monitoring plans before deployment, with documentation retained for at least 10 years.

How do auditors assess AI governance compliance?

Auditors look for operational evidence: named owners with documented authority, active audit logs, risk approval records, and control enforcement history. Written governance policies without operational evidence do not satisfy regulatory examination requirements.